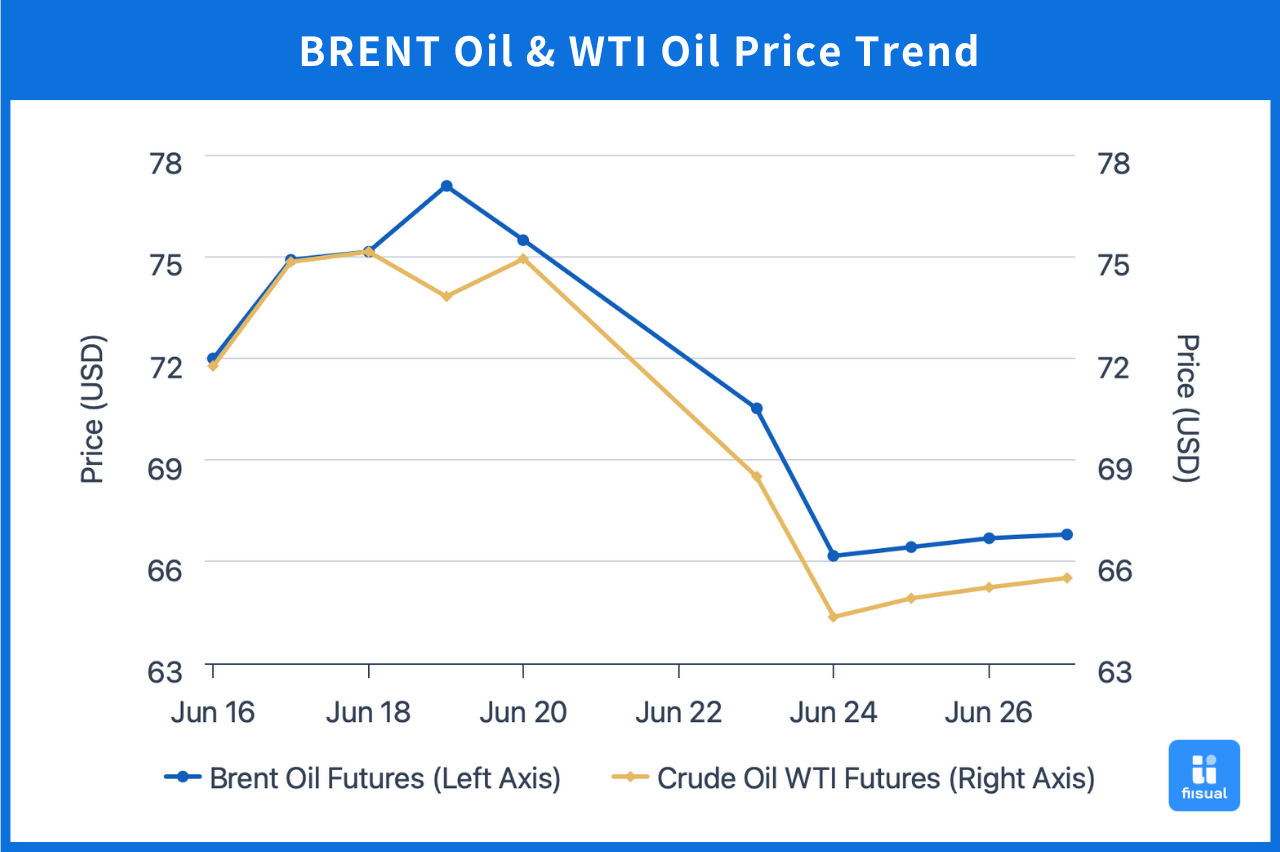

Price Trend Summary

| June 30 Open | July 11 Close | Price Change | |

|---|---|---|---|

| Brent Crude | 67.33 | 70.36 | +4.50% |

| WTI Crude | 65.15 | 68.45 | +5.07% |

| Dubai Crude | 69.27 | 70.78 | +2.18% |

In the first week, Houthi and Hamas forces launched missile attacks on Israel, escalating geopolitical risks and lifting oil prices. Midweek, EIA reported unexpected builds in crude and gasoline inventories, raising concerns over driving season demand and pushing prices down. Later, Iran announced the suspension of cooperation with the IAEA and partially closed its airspace, further heightening tensions and driving prices back up.

In the second week, tightening spot market fundamentals and Saudi Arabia’s hike in August OSPs to Asia signaled confidence in demand and supported price gains. Later in the week, oil prices briefly fell on Trump’s tariff policy news, but rebounded again as the IEA monthly report reiterated market tightness and U.S.-EU sanctions on Russia intensified.

Crude Oil Data Update

Crude Inventories Rebound; Refined Product Draws Slow; Upstream Investment Remains Weak

| Jul 9, 2025 | Jul 2, 2025 | Jun 25, 2025 | |

|---|---|---|---|

| Inventories (mn bbls) | |||

| Commercial Crude (ex-SPR) | 426.0 (+7.0) | 419.0 (+3.9) | 415.1 |

| SPR | 403.0 (+0.2) | 402.8 (+0.3) | 402.5 |

| Gasoline | 229.5 (-2.6) | 232.1 (+4.2) | 227.9 |

| Distillates | 102.8 (-0.8) | 103.6 (-1.7) | 105.3 |

| Production Activity | |||

| Rig Count | 425 (-7) | 432 (-6) | 438 |

| Refinery Utilization (%) | 94.7 (-0.2) | 94.9 (+0.2) | 94.7 |

Over the past two weeks, U.S. commercial crude inventories increased by a significant 10.9 million barrels, far exceeding market expectations. However, inventory levels remain relatively low and within healthy ranges. The SPR rose slightly by 0.5 million barrels, continuing its slow but steady replenishment. On the refined products side, gasoline inventories rose by 1.6 million barrels, which may raise concerns over driving season demand. Distillate inventories fell by 2.5 million barrels, indicating continued robust demand for diesel and jet fuel.

On the supply side, the U.S. active rig count dropped sharply by 13 units, confirming a trend of softening shale output in the coming months. However, some shale producers had hedged with high-priced put options during the earlier oil rally, providing short-term cost protection, which could limit further declines in rig counts. Refinery utilization remained elevated, as refiners continued to stock up during peak season.

Agency Reports

- EIA: The EIA revised down its 2025 U.S. crude supply forecast from 13.42 mb/d to 13.37 mb/d due to the continued decline in active rigs. It attributed the slowdown in drilling and completion activity to higher steel prices, tariff pressures, and reduced capital spending. On pricing, the EIA raised its 2025 Brent forecast by $3 to $69/bbl due to geopolitical risk premiums, while the 2026 forecast was slightly lowered by $1 to $58/bbl due to expected inventory builds.

- IEA: The IEA slightly downgraded its 2025 global oil demand growth forecast to 700 kb/d, the lowest since 2009 excluding the pandemic in 2020, citing weak emerging market demand. On the supply side, the IEA raised its forecast in response to OPEC’s plan to accelerate output from August. While the supply-demand gap widened, the IEA noted that higher refinery utilization driven by summer driving and power generation needs has kept the physical market tight, and current conditions do not reflect oversupply.

Note:

- EIA forecasts do not factor in OPEC's August production increases.

- Neither agency has incorporated the potential demand boost from the “Big and Beautiful” Act.

Supply and Demand Table (OPEC not yet updated)

| Unit: mb/d | Supply | Demand | |||||

|---|---|---|---|---|---|---|---|

| Agency | EIA | OPEC (non-DoC liquids + DoC NGLs) | IEA | EIA | OPEC (OECD) | OPEC (non-OECD) | IEA |

| 2024 | 102.80 | 61.5 | 103.04 | 102.74 | 45.67 | 58.17 | 102.90 |

| 2025 | 104.61 (+0.26) | 62.4 | 105.10 (+0.3) | 103.54 (+0.01) | 45.83 | 59.31 | 103.60 (-0.02) |

| 2026 | 105.72 (+0.58) | 63.3 | 106.40 (+0.4) | 104.59 (+0.01) | 45.91 | 60.51 | 104.32 (-0.04) |

International Developments

“Big and Beautiful” Act Passed

On July 4 (local time), Trump signed the “Big and Beautiful” Act into law. The act loosens federal land restrictions for oil and gas drilling and calls for large-scale lease auctions in the Gulf of Mexico and several states. It also lowers royalty rates and related extraction costs, expected to significantly boost U.S. oil production capacity and supply flexibility. On the demand side, the act reduces subsidies for renewables and EVs, favoring traditional vehicles and fossil-fueled power, potentially boosting mid-term oil demand and supporting prices.

OPEC Expands Production Increase

On July 5 (local time), OPEC+ announced a 548 kb/d production increase starting August, higher than the previous 411 kb/d. The decision reflects a strong global economic outlook, robust Northern Hemisphere summer demand, and low global inventories.

The market had expected OPEC to maintain the previous pace. The larger-than-expected hike could exert short-term pressure on prices. However, given the decline in U.S. rig counts and limited supply growth from non-OPEC countries, the overall supply shock should remain relatively moderate.

Commentary

Oil prices have shown remarkable resilience recently. OPEC’s expanded production has not dragged prices down, indicating that markets expect strong demand to absorb the additional supply. In the short term, spot market fundamentals remain the key price driver. Refined product inventory movements and refinery utilization rates are important indicators to watch for signs of weakening demand.

In the medium term, the “Big and Beautiful” Act is expected to gradually drive oil demand and potentially delay the U.S. energy transition, supporting long-term oil prices. Going forward, tariff developments, U.S. macro data, and Western sanctions on Russia will be key areas to monitor.

Summary

While the spot market continues to support oil prices in the short term, the overall market still lacks clear upward momentum. Despite an unexpected crude inventory build in the U.S., overall levels remain low and within a healthy range. Watch for any abnormal refined product stock builds to gauge potential demand weakness. In the medium term, the “Big and Beautiful” Act could reshape supply-demand dynamics and introduce new volatility.