Apple Raises Product Prices as Memory Costs Surge

Apple, the global smartphone leader, announced on June 25 that it would raise prices for several products, including Macs and iPads, with increases reaching double digits. The primary driver is the sharp rise in memory prices, which has significantly increased costs for consumer electronics manufacturers. Apple CEO Tim Cook stated that memory suppliers are passing substantial cost increases down the supply chain, leaving Apple with little choice but to raise product prices.

Apple is not alone. Microsoft has also announced a price increase for Xbox consoles effective August 1, while major PC brands Lenovo, HP, and Dell had already begun notifying global consumers as early as late April of either price increases or reductions in memory configurations. These developments suggest that the current wave of price hikes is not an isolated decision by a single brand, but rather a reflection of the structural cost pressures facing the entire consumer electronics industry following the sharp increase in memory costs.

| Product | Previous Price (USD) | New Price (USD) | Increase |

|---|---|---|---|

| MacBook Neo (Entry Model) | $599 | $699 | +16.7% |

| 13-inch MacBook Air | $1,099 | $1,299 | +18.2% |

| 14-inch MacBook Pro | $1,699 | $1,999 | +17.6% |

| 16-inch MacBook Pro | $2,699 | $2,999 | +11.1% |

| iMac (Entry Model) | $1,299 | $1,499 | +15.4% |

| 11-inch iPad Air | $599 | $749 | +25.0% |

| 13-inch iPad Air | $799 | $949 | +18.8% |

| iPad Pro | $999 | $1,199 | +20.0% |

| HomePod | $299 | $349 | +16.7% |

| HomePod mini | $99 | $129 | +30.3% |

| Apple TV | $149 | $199 | +33.6% |

| Vision Pro | $3,499 | $3,699 | +5.7% |

| iPhone / Apple Watch / AirPods | — | No Change | — |

Table 1. Price Increases Across Apple's Product Lineup Source: Pocket Securities, Apple Online Store Announcement (June 25, 2026), 9to5Mac, Bloomberg

The Consumer Memory Market Imbalance Is Closely Linked to the Industry's Supply Structure

The imbalance in the consumer memory market is fundamentally tied to the structure of memory supply. In consumer electronics, memory mainly consists of DRAM and NAND Flash, which are responsible for system memory and data storage, respectively. These memory technologies are widely used in servers, PCs, smartphones, and data centers. Together, they account for the vast majority of global memory revenue and shipments, meaning changes in their supply and demand directly affect the cost structure and supply stability of the broader consumer electronics industry.

Readers interested in this topic may also find our previous articles helpful:

Samsung, SK hynix, and Micron Face Antitrust Lawsuit: Is AI Driving a Memory Supply Squeeze?

Industry 101: Introduction to Memory

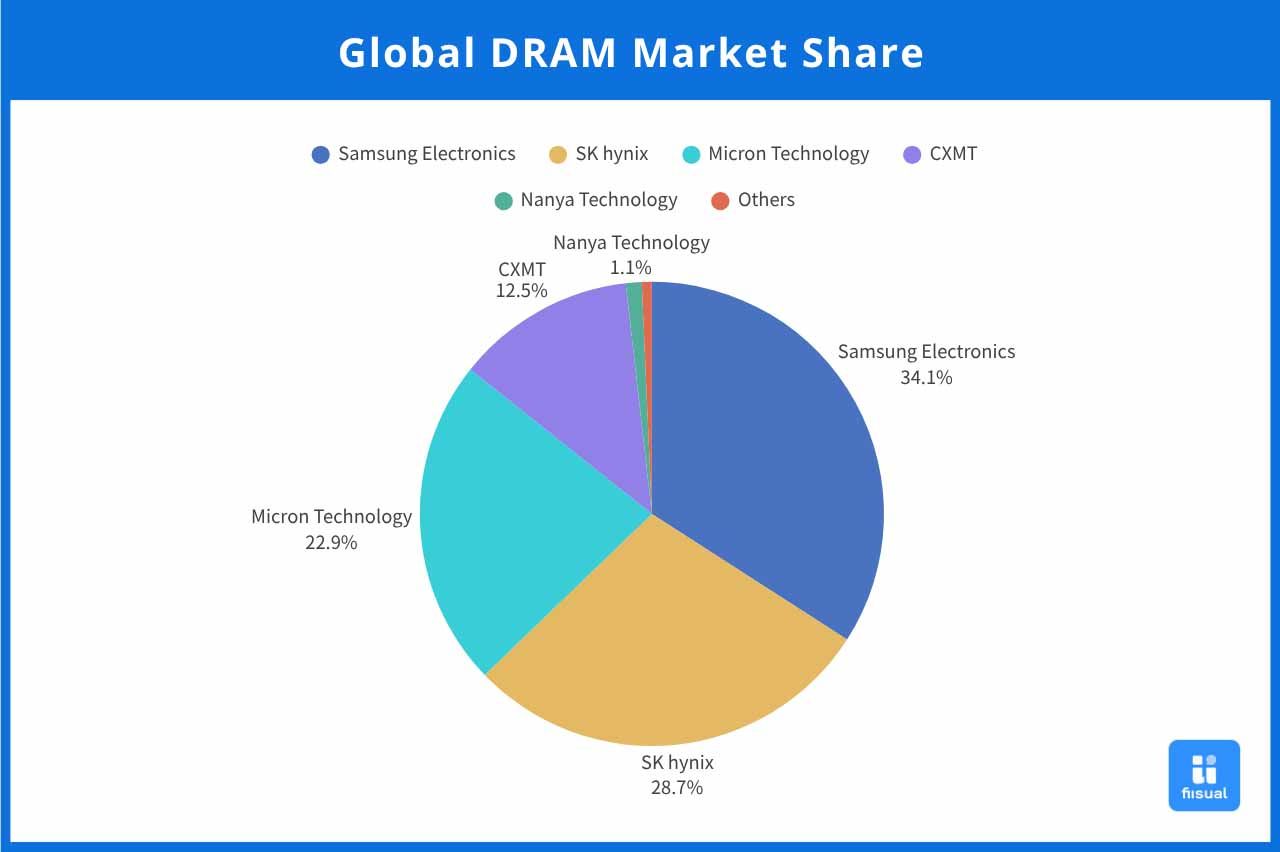

The Global DRAM Market Is Dominated by Three Major Suppliers

Source: Gartner

Source: Gartner

DRAM is a core component of modern computing, offering high-speed data access and high bandwidth. Whether in servers, PCs, laptops, or smartphones, all systems rely on DRAM as system memory to run operating systems and applications.

The global DRAM market is largely controlled by Samsung Electronics, SK hynix, and Micron Technology because the industry is highly capital-intensive, technology-intensive, and driven by economies of scale. DRAM manufacturing requires enormous investments in semiconductor fabrication facilities while continuously advancing process technology, node scaling, yield management, and manufacturing integration, creating exceptionally high barriers to entry.

At the same time, DRAM is a highly standardized product whose pricing is heavily influenced by supply-demand cycles. Past downturns have caused significant earnings volatility across the industry, gradually forcing manufacturers without sufficient cost advantages or financial strength to exit or consolidate. As manufacturing complexity and capital requirements continue to increase, market concentration has risen further, with the top three suppliers still controlling more than 80% of global market share, maintaining a highly concentrated industry structure.

NAND Has More Diverse Applications and a Broader Supply Chain Than DRAM

Source: Gartner

Source: Gartner

NAND Flash is primarily used for long-term data storage and offers advantages in storage capacity, cost efficiency, and data retention. Its applications include consumer SSDs, smartphone and tablet storage, embedded storage for automotive and industrial equipment, and enterprise SSDs deployed in data centers.

Compared with DRAM, the NAND market has more suppliers because its applications and product types are more diverse. Products can be differentiated by capacity, cost, read/write performance, controller design, and end-use applications, while downstream participation from module manufacturers and branded vendors is also much broader.

Major suppliers include Samsung Electronics, SK hynix, Kioxia, Micron Technology, SanDisk, and Yangtze Memory Technologies Co. (YMTC). Although the NAND market also exhibits an oligopolistic structure, its broader application base and more diversified value chain allow for greater supplier participation than the DRAM market.

AI Demand Is Crowding Out Consumer Memory Capacity and Worsening Supply Imbalances

Beyond the concentration of supply among a handful of manufacturers, the rapid expansion of AI applications has further intensified the imbalance in the memory market.

As data centers dramatically increase demand for training and inference workloads for large AI models, demand for high-speed, high-bandwidth data transmission has surged, driving rapid growth in High Bandwidth Memory (HBM). Since HBM generates gross margins roughly three to five times higher than conventional DRAM, Samsung Electronics, SK hynix, and Micron Technology have continued reallocating wafer capacity toward HBM production.

Because these three manufacturers account for most of the world's DRAM supply, prioritizing HBM production significantly reduces the capacity available for conventional products such as DDR4, DDR5, and Mobile DRAM. This has created a crowding-out effect, making it increasingly difficult for supply to keep pace with demand for traditional DRAM products.

At the same time, AI data center construction has significantly increased storage demand, leading to shortages of hard disk drives (HDDs). Due to years of limited capacity expansion and relatively long production lead times, HDD manufacturers have struggled to meet rapidly rising demand. As a result, major cloud service providers (CSPs) have increasingly turned to enterprise SSDs as alternatives, pushing enterprise SSD demand well above market expectations.

Because enterprise SSDs generally offer higher profit margins than consumer SSDs, the NAND market has experienced a capacity crowding-out effect similar to that seen in DRAM.

Meanwhile, after previous periods of aggressive capacity expansion led to oversupply and sharp declines in industry profitability, NAND manufacturers have adopted more conservative capital spending strategies since late 2024. Most suppliers have reduced wafer starts and postponed new capacity additions to avoid another price collapse caused by oversupply, further tightening today's market.

The combination of capacity crowding, rapidly rising demand, and cautious expansion strategies has driven DRAM and NAND prices sharply higher for several consecutive quarters.

According to TrendForce, memory prices in the first quarter of 2026 increased by 80% to 90% compared with the fourth quarter of 2025. The research firm also forecasts that conventional DRAM contract prices will rise another 58% to 63% quarter over quarter in the second quarter, while NAND Flash prices are expected to increase 70% to 75%.

Looking over a longer period, commercial DRAM prices have surged roughly 700% since 2022. In the consumer market, Mobile DRAM used in smartphones rose 78% in a single quarter, while SSD prices for laptops doubled within a year, sharply increasing costs for downstream manufacturers.

Chinese Memory Makers Are Expanding Rapidly with Government Support

Against the backdrop of severe global memory shortages, China's memory market has gradually evolved into a relatively independent supply-demand ecosystem focused primarily on domestic demand, largely due to U.S. export restrictions.

Although AI-driven demand has accelerated globally since the pandemic, leading international manufacturers have generally remained cautious about expanding production capacity. In contrast, supported by government policies aimed at strengthening domestic semiconductor self-sufficiency, Chinese memory manufacturers have aggressively expanded capacity, with ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies Co. (YMTC) emerging as the leading examples.

ChangXin Memory Technologies Is China's Only Large-Scale DRAM IDM

Founded in 2016, ChangXin Memory Technologies (CXMT) is China's only integrated device manufacturer (IDM) capable of large-scale DRAM production. The company focuses on the design, development, manufacturing, and sales of DRAM chips.

CXMT currently operates three 12-inch wafer fabs in Hefei and Beijing and is constructing an HBM packaging facility in Shanghai. Its product portfolio mainly consists of DDR4 and DDR5 memory, with sales primarily serving domestic Chinese customers.

Although relatively young, CXMT has expanded rapidly following U.S. export controls on China's semiconductor industry. Recognized as a strategic national asset under China's technology and information security initiatives, the company has received strong policy and financial support.

Between 2021 and 2025, CXMT's monthly wafer capacity grew at a 51% compound annual growth rate (CAGR) to 173,000 wafers per month, making it the world's fourth-largest DRAM supplier after Samsung Electronics, SK hynix, and Micron Technology.

| Thousand Wafers per Month | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Samsung | 584 | 653 | 527 | 614 | 655 |

| SK Hynix | 356 | 393 | 352 | 416 | 528 |

| Micron | 355 | 353 | 278 | 314 | 333 |

| CXMT | 50 | 54 | 90 | 173 | 260f |

Table 2. Monthly Wafer Capacity of Major Global DRAM Suppliers (2021–2025)

Source: TrendForce

YMTC Expanded Through the Downturn and Secured a Strong Position in NAND

Founded in 2016 through investments from Tsinghua Unigroup and the Chinese government, Yangtze Memory Technologies Co. (YMTC) focuses on memory manufacturing, with its core business centered on the design, development, production, and sales of 3D NAND Flash.

In addition to manufacturing 3D NAND wafers and storage products, the company markets enterprise SSDs under its own brand while selling consumer storage products through its ZhiTai brand, primarily serving domestic Chinese customers.

Before AI demand accelerated, major manufacturers had expected NAND demand to soften alongside slowing consumer electronics sales and therefore reduced production to stabilize prices and profitability.

However, supported by China's semiconductor localization strategy, YMTC expanded capacity during the industry downturn. As a result, the company has become one of China's leading NAND suppliers, with wafer production surpassing Micron Technology in 2025, making it the world's fourth-largest NAND supplier.

| Annual Capacity Growth (%) | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Samsung | 11 | (23) | (3) | (12) |

| Kioxia/Sandisk | (4) | (17) | 12 | (10) |

| SK Hynix | 50 | (20) | (8) | 8 |

| Micron | (1) | (21) | 7 | (9) |

| YMTC | 47 | 23 | 4 | 18 |

| Global | 11 | (18) | 2 | (5) |

Table 3. Annual Capacity Growth of Major Global NAND Suppliers (2022–2025)

Source: TrendForce

Despite U.S. Restrictions, Chinese Memory Makers Continue Closing the Gap

Due to concerns over government involvement in corporate operations, the United States has added multiple Chinese technology companies to export control lists and the Department of Defense's Section 1260H list. These measures restrict exports of the most advanced semiconductor equipment to China and may also limit purchases by certain overseas customers.

Despite these restrictions, Chinese memory manufacturers continue advancing through strong government support and investment. Production capacity has steadily approached that of leading international suppliers, while technological gaps continue to narrow.

For example, CXMT has already entered mass production of DDR5 products and begun HBM development. Meanwhile, YMTC continues advancing its 3D NAND technology, demonstrating meaningful progress in both product generations and advanced memory technologies.

Overall, while U.S. export controls have limited China's access to cutting-edge equipment and overseas markets, government-backed localization initiatives and strong domestic demand continue to support expansion and technological advancement, positioning Chinese suppliers to play an increasingly important role in the global memory industry.

Apple's Strategic Procurement of Chinese Memory Strengthens Its Negotiating Position

Apple Reportedly Plans to Source DRAM from CXMT, Though Near-Term Impact May Be Limited

As AI-related demand absorbs an increasing share of memory supply, consumer electronics manufacturers have been forced to accept higher prices to secure shipments. In the short term, companies can only absorb rising costs or pass them on to consumers through higher retail prices.

However, as memory prices continue climbing, manufacturers are finding it increasingly difficult to sustain higher costs over the long term, prompting them to seek alternative suppliers and additional cost-control measures.

With Chinese memory manufacturers gradually closing the technology and production gap with the industry's three dominant suppliers, some customers have begun evaluating procurement opportunities.

As a leading consumer electronics company, Apple has reportedly taken the first step by considering the purchase of DRAM from ChangXin Memory Technologies (CXMT) to reduce its dependence on existing suppliers.

However, the move is expected to have only a limited impact on the memory market in the near term for several reasons.

1. Geopolitical Risks

CXMT remains on the U.S. Department of Defense's Section 1260H list. Although there had been speculation that the company might be removed, it remained on the latest list released in June.

While inclusion on the list does not constitute a direct export ban, it does trigger heightened supply chain scrutiny. Apple would therefore need to navigate U.S. regulatory oversight and supply chain compliance requirements before adopting CXMT products.

2. CXMT Products Have Yet to Meet Apple's Highest Technical Standards

As one of the world's leading consumer electronics brands, Apple maintains exceptionally stringent component requirements.

For memory, Apple's specifications require LPDDR5X transmission speeds exceeding 10 Gbps while operating at approximately 1.1V.

Although CXMT's LPDDR5X products have achieved industry-standard speeds, limitations resulting from restricted access to advanced manufacturing equipment mean that capacitor performance and leakage current remain less competitive. As a result, power efficiency and thermal performance may still fall short of the demanding requirements for flagship iPhone models.

3. Patent Litigation Risks

Core DRAM intellectual property has long been dominated by Samsung Electronics, SK hynix, and Micron Technology.

If Apple were to adopt CXMT products on a large scale, it could potentially face third-party patent infringement claims, increasing legal costs and supply chain uncertainty.

Apple's Move Is About Negotiating Leverage, Not Shifting Its Supply Chain

Given these constraints, Apple's reported interest in CXMT is unlikely to represent an effort to replace Samsung Electronics, SK hynix, and Micron Technology as its primary memory suppliers. Rather, the strategy appears intended to establish Chinese DRAM suppliers as potential qualified vendors, strengthening Apple's bargaining position during negotiations for its 2027 supply agreements.

By introducing an alternative sourcing option, Apple may gain additional leverage to negotiate lower prices and reduce premiums associated with urgent supply orders.

With AI demand continuing to tighten consumer memory supply and contract prices rising rapidly, simply having a credible alternative supplier can improve Apple's negotiating position.

Combined with Apple's enormous purchasing scale, economies of scale, and strong brand influence, this strategy could further widen Apple's competitive advantage over other smartphone manufacturers and may encourage additional consumer electronics companies to pursue similar approaches.

Conclusion

Overall, the current surge in memory prices is not a temporary event or the result of actions by any single company. Instead, it reflects a structural supply-demand imbalance driven by rapidly expanding AI demand, highly concentrated memory production, and manufacturers shifting capacity toward higher-margin products such as HBM and enterprise SSDs.

As DRAM and NAND are essential components in virtually all consumer electronics, rising memory costs have already affected Apple, Microsoft, and leading PC manufacturers, forcing downstream companies to respond through price increases, lower product specifications, or alternative sourcing strategies.

For Apple, sourcing DRAM from ChangXin Memory Technologies does not signal a broad supply chain shift in the near term. Instead, it appears to be a strategic effort to introduce a potential alternative supplier, thereby strengthening its negotiating position in 2027 supply contract discussions and reducing the impact of rising memory costs on product margins and pricing.

If tight memory supply conditions persist, Chinese suppliers are likely to continue expanding their influence within the global memory industry, potentially reshaping the balance of negotiating power between consumer electronics brands and traditional memory manufacturers.