In capital markets, investors make decisions based on their own judgment of a target company’s stock price. Many investors, when facing price fluctuations, tend to rely on historical prices or their own purchase price as reference points. However, the investment world offers a comprehensive and systematic set of valuation methodologies that help investors quantify their views, moving beyond intuition-driven reactions to price movements. By incorporating multiple assumptions into valuation models and grounding analysis in research, investors can build a consistent and structured framework, enabling more precise investment decisions.

What Is a Company’s True Value?

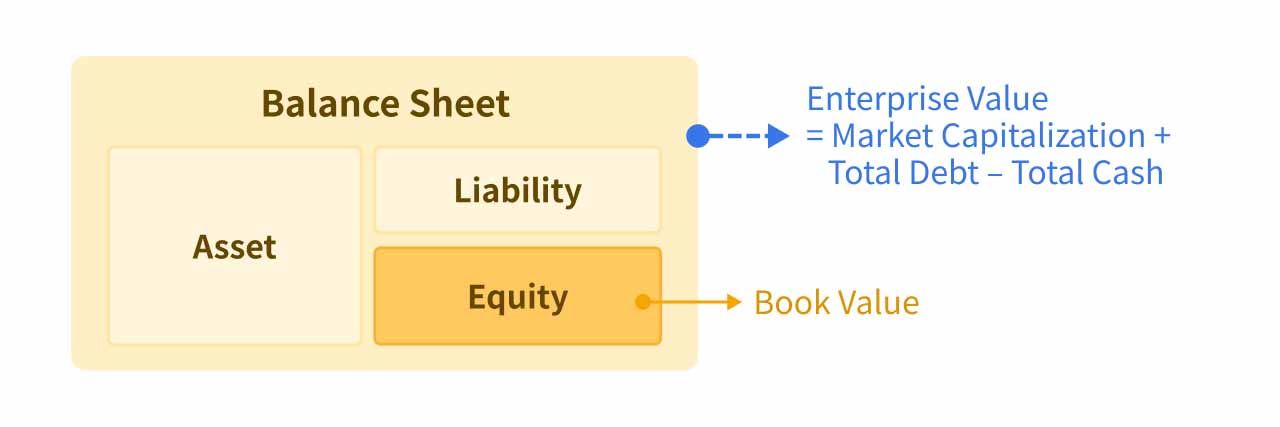

From an accounting perspective, a company’s value can first be measured using figures from its financial statements, such as shareholders’ equity on the balance sheet, commonly referred to as book value (BV). From a capital markets perspective, however, the market typically evaluates a company based on equity market capitalization plus net debt, known as enterprise value (EV)—which can be seen as the theoretical cost of acquiring the entire business.

You can also find more here: Financial Report 101: Introduction to the Balance Sheet

That said, a company’s true worth is often neither equal to its accounting book value nor necessarily reflected in its current market price. Market prices may deviate from a company’s intrinsic value due to information asymmetry, investor sentiment, or misjudgment of future prospects. One of the core assumptions of value investing is that while market prices may diverge from intrinsic value in the short term, they tend to converge toward it over the long run. Therefore, if investors can assess a company’s value more accurately than the market, they may profit from the gap between price and intrinsic value.

For both investors and corporate managers, understanding and estimating a company’s intrinsic value carries significant business implications. For investors, if they can more accurately determine a listed company’s intrinsic value than the broader market, they can compare it with the company’s current market capitalization. When a meaningful gap exists, it may present an actionable investment opportunity and potential returns from price convergence.

In theory, the closer an investor’s valuation estimate is to intrinsic value, the greater the likelihood of generating excess returns. For example, in long-only equity investing, a key task for institutional investors, analysts, and researchers is to identify stocks whose prices deviate from intrinsic value. By analyzing financial statements, industry trends, competitive dynamics, and other available information, they develop valuation views that may challenge market consensus. When analysts believe a company’s intrinsic value exceeds its current market price, they may conclude that the stock is undervalued, forming the basis for a buy recommendation.

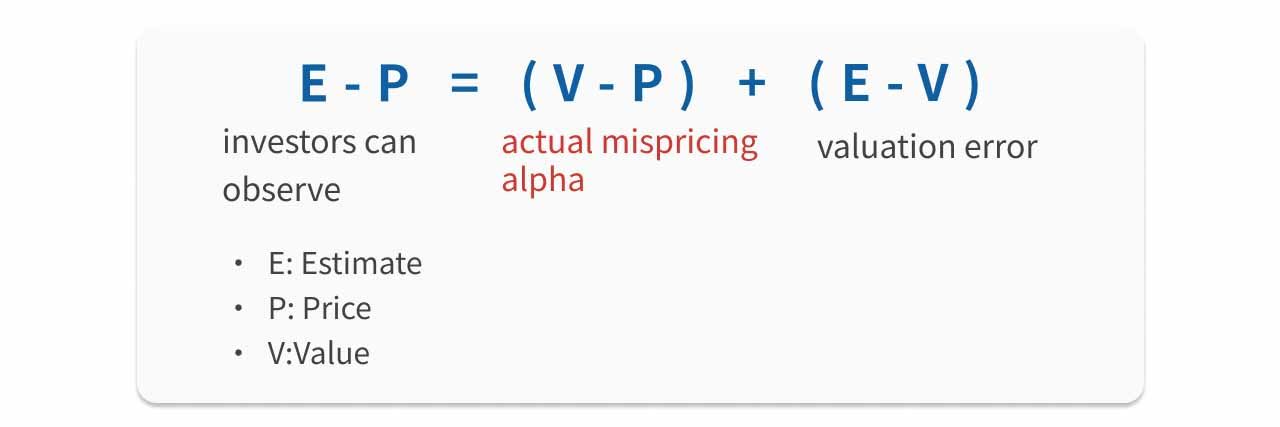

Returns generated from accurately estimating intrinsic value and capturing the gap between price and value are commonly referred to as abnormal returns, or alpha.

In notation, let E (Estimate) represent the analyst’s estimated value, P (Price) the market price, and V (Value) the true intrinsic value. The actual mispricing is V − P, while what investors can observe and act upon is E − P. The difference lies in the fact that the analyst’s estimate may not perfectly match intrinsic value.

However, this framework relies on a key assumption: market prices will eventually converge to intrinsic value. In reality, capital markets are uncertain. Even if analysts correctly identify mispricing, the market may not adjust immediately. Price convergence may take time—or may not occur within the investment horizon at all.

As a result, for active investors, simply identifying whether a stock is overvalued or undervalued is often not sufficient. Beyond spotting mispricing, they also look for events that could shift market perception and prompt a reassessment of a company’s fundamentals and outlook, thereby driving price convergence. Such events may include earnings surprises, new product launches, industry upcycles, or M&A activity. These events are commonly referred to as catalysts.

How to Calculate a Company’s Intrinsic Value

Estimating Value Through Financial Models

In practice, analysts estimate a company’s intrinsic value by forecasting its future financial performance. A financial model essentially reconstructs a company’s future financial statements, covering periods ranging from a few quarters to several years. However, accurate valuation cannot rely solely on extrapolating historical revenue or profit figures. Analysts must first develop a deep understanding of the business, including its macroeconomic and industry environment, competitive landscape, strategy, business model, and historical performance.

Building Core Assumptions

After gathering this information, analysts translate qualitative insights into quantifiable and testable inputs—a process known as building assumptions. These assumptions form the foundation of financial models and serve as the bridge between complex information and a structured valuation framework. Based on projected financials, analysts then derive enterprise value and fair stock price—this process is known as valuation. The quality of assumptions is therefore critical and often determines the usefulness of the model.

Understanding Business Models and Profitability

Analysts must also understand how a company makes money—its business model. This includes identifying its customers, products or services, value delivery mechanisms, and operational structure. Through financial analysis, they assess execution effectiveness and further evaluate profitability, cash flow generation, capital efficiency, and risk levels.

Identifying Competitive Advantages (Moats)

With a solid understanding of the company, analysts conduct competitive analysis to determine whether the firm can sustain superior returns and stable cash flows relative to peers. Such advantages may stem from brand strength, switching costs, cost leadership, or economies of scale—commonly referred to as a company’s moat. Valuation analysis thus helps not only assess whether a stock is fairly priced but also compare investment attractiveness across companies.

In practice, analysts rely on a wide range of information sources beyond financial statements, including regulatory filings, corporate disclosures, press releases, investor relations materials, and management discussions. Cross-verifying multiple sources and building a consistent analytical framework is essential to systematically estimating intrinsic value.

Main Types of Valuation Models

After forecasting financial performance, analysts select appropriate valuation methods to translate operational and financial expectations into value estimates. Common approaches include absolute valuation, relative valuation, asset-based valuation, and specialized models for specific situations.

Each method has different assumptions, applications, and analytical focuses; no single model fits all companies or industries. Understanding these frameworks is key to building a robust valuation toolkit.

| Valuation Method | Absolute Valuation | Relative Valuation | Asset-Based Valuation | Other Specialized Models |

|---|---|---|---|---|

| Core Principle | Values a company based on the present value of future cash flows, earnings, or dividends. | Uses valuation multiples of comparable companies or transactions to estimate fair value. | Assesses value based on the company’s current assets and liabilities. | Applies specific financial logic for unique situations such as complex capital structures or transactions. |

| Common Methods | DCF, Dividend Discount Model (DDM), Residual Income Model | P/E, P/B, P/S, EV/EBITDA, EV/EBIT, comparable company and transaction analysis | Book value, adjusted net asset value, replacement cost, liquidation value | LBO models, SOTP, M&A accretion/dilution analysis, real options valuation |

| Typical Use Cases | Stable, predictable businesses with reliable cash flows | Situations with sufficient peer comparisons; often used for quick checks | Asset-heavy sectors such as financials or real estate, or liquidation scenarios | Private equity deals, conglomerates, M&A, or high-uncertainty projects |

Case Study: NVIDIA

Taking NVIDIA as an example, analysts typically begin by understanding its industry positioning and business model. NVIDIA is now widely viewed as an AI and data center–focused accelerated computing platform company, with operations spanning data centers, gaming GPUs, professional visualization, and automotive computing. In recent years, AI and data centers have become its primary growth drivers.

From a competitive standpoint, NVIDIA faces different rivals across segments. In data center/AI, competitors include Advanced Micro Devices, Inc. (AMD), Intel Corporation (Intel), and ASIC providers. In gaming GPUs, competition mainly comes from AMD and Intel. In data center interconnect and networking, competitors include Broadcom Inc. (Broadcom) and Marvell Technology, Inc. (Marvell). This means analysts must evaluate NVIDIA as a multi-product platform company rather than focusing on a single product line.

In terms of its business model, NVIDIA goes beyond selling GPUs. It offers a full-stack AI infrastructure solution encompassing GPUs, CPUs, DPUs, networking, systems, and software platforms. Therefore, financial modeling must consider not only chip shipments and pricing but also data center demand, system-level procurement, and software-driven revenue expansion.

NVIDIA’s competitive moat is also significant. Its CUDA software ecosystem creates strong developer lock-in and switching costs, while its full-stack integration—from chips to systems—strengthens its position in AI infrastructure. These factors influence the valuation multiples investors are willing to assign.

Analysts also monitor potential catalysts, such as new platform rollouts, rising inference demand, or increased enterprise AI adoption, as these can drive market re-rating. Based on industry analysis, competitive positioning, and assumptions, analysts ultimately derive fair value and target price through valuation models.

Conclusion

Valuation does not begin with models, but with understanding how a business creates value. Financial models are tools that translate insights about business models, industry structure, competitive advantages, and financial logic into a structured and testable framework. The true value of valuation lies not in the model itself, but in the quality of the underlying assumptions and business understanding.

As the starting point of the “Valuation Model Fundamentals” series, this article addresses two key questions: where company value comes from, and what role financial models play in analysis. Clarifying these foundations helps avoid mechanical formula application and ensures a return to the essence of business analysis.

There is no single correct answer in valuation. Different industries, business models, and life cycle stages require different approaches. The key is understanding which methods to use in which context, identifying critical assumptions, distinguishing outputs from drivers, and recognizing the core variables that truly determine value.

In upcoming sections, this series will break down essential fundamentals before building financial models, including the linkage between financial statements, differences between accounting figures and actual cash flows, and how to identify key revenue drivers and cost structures based on business models.

Related Articles: