Uber, Lucid, Nuro Robotaxi in operation.

At CES 2026 in the United States, Uber, Lucid, and Nuro jointly unveiled their autonomous taxi. This Robotaxi is built on Lucid’s all-electric Gravity SUV platform, equipped with Nuro’s Level 4 autonomous driving technology, and integrated with Uber’s global mobility platform. Lucid plans to mass-produce the Robotaxi in Arizona. If testing and early operations progress smoothly, Uber aims to deploy up to 20,000 Gravity SUV Robotaxis across dozens of global markets over the next six years. Each company plays a distinct role in the partnership:

- Uber: Responsible for platform operations and fleet management, including remote assistance, charging, cleaning, maintenance, customer service, and integration of dispatch systems, dynamic pricing, and its global network

- Lucid: Supplies the electric vehicle hardware (Lucid Gravity SUV), positioned in the premium business segment, emphasizing long driving range and a spacious, comfortable cabin

- Nuro: Provides Level 4 autonomous driving software (Nuro Driver) and oversees real-world road testing, system validation, and safety assessments

Real-world road testing led by Nuro began in San Francisco in December last year, with safety operators monitoring the vehicles throughout. Commercial services are expected to launch in the San Francisco Bay Area in the second half of 2026. The vehicles feature 360-degree environmental perception, integrating high-resolution cameras, solid-state lidar, and radar to ensure real-time, precise awareness under diverse traffic and weather conditions.

On the computing side, the Robotaxi uses NVIDIA’s DRIVE AGX Thor chip to handle real-time AI computing, sensor fusion, and system integration. In addition, the roof-mounted low-drag module known as “Halo” integrates sensors and LED lighting that can display passenger initials and real-time status alerts, helping riders quickly identify the correct vehicle and providing clear visual feedback.

This partnership also signals a major shift in the Robotaxi business model—from highly vertically integrated approaches (such as early Waymo or Cruise) to an open ecosystem built on horizontal specialization among EV manufacturers, autonomous driving technology providers, and ride-hailing platforms.

Uber’s Transformation into a Robotaxi Ecosystem Integrator

In 2015, Uber attempted to develop its own autonomous driving technology. After committing significant capital, the company faced technological bottlenecks, safety incidents, and legal risks. In December 2020, Uber sold its Advanced Technologies Group (ATG) to Aurora, committed an additional $400 million investment, and received approximately a 26% stake in Aurora—formally ending its in-house autonomous driving strategy.

Uber’s partnerships with at least 21 companies in recent years—covering autonomous passenger vehicles, trucks, and delivery robots—highlight a clear strategic shift. Rather than trying to become a car manufacturer or autonomous technology developer, Uber is now securing stable autonomous vehicle supply through investments and partnerships, positioning itself as an integrator on both the supply and demand sides.

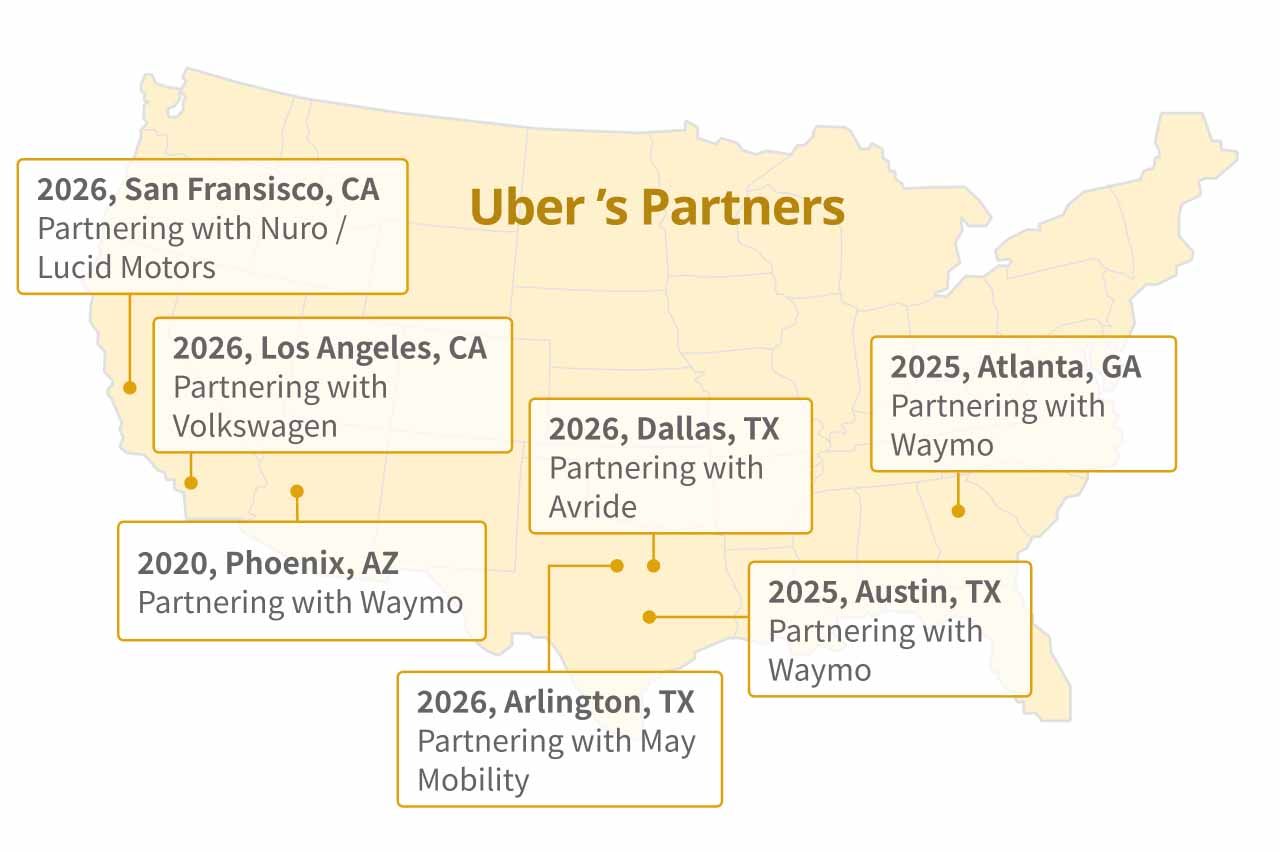

By the end of 2025, Uber had achieved autonomous operations in four cities, pilots in three more, and stated plans to launch driverless services in over 10 markets by the end of 2026.

Uber’s Key Partners

Waymo

Uber and Waymo have launched Robotaxi ride services in multiple U.S. cities, including Austin and Atlanta. Riders can book Waymo vehicles directly through the Uber app. Currently, there are around 200 Waymo vehicles on Uber’s platform in Austin and about 100 in Atlanta. Uber handles dispatch and platform integration, while Waymo retains technological leadership and testing responsibility.

Volkswagen ADMT

The two companies plan to launch the autonomous ID. Buzz on Uber’s platform in 2026, with initial operations in Los Angeles. Volkswagen will deliver an initial batch of 480 Robotaxis to Uber, as part of a potential order totaling up to 10,000 vehicles.

BYD

Uber announced a partnership with BYD to introduce 100,000 BYD electric vehicles onto the Uber platform, lowering acquisition costs for Uber drivers and jointly developing autonomous driving technology. The initiative will start in Europe and Latin America, with plans to expand to the Middle East, Canada, Australia, and New Zealand. Thanks to lower maintenance costs, a broad model lineup, and strong battery performance, BYD vehicles are well suited for shared electric mobility.

Momenta

Uber and Chinese autonomous driving company Momenta announced plans to conduct Level 4 Robotaxi testing in Germany this year, marking Uber’s formal expansion of Robotaxi operations into Europe and supporting integration with local regulations, vehicle standards, and consumer behavior.

Baidu Apollo Go

Uber plans to launch a pilot program in London in the first half of 2026 using Baidu Apollo Go’s RT6 model, with full commercial operations expected by year-end.

Avride

Uber is partnering with Avride, an autonomous vehicle subsidiary of Nebius, to launch autonomous mobility services in Dallas. The two sides plan to invest up to $375 million to accelerate fleet expansion, targeting up to 500 vehicles.

Nvidia, Stellantis

Uber provides selected real-world driving data to Nvidia to help improve AI models and chip technology. By 2027, the partnership aims to gradually deploy a fleet of 100,000 autonomous vehicles powered by Nvidia DRIVE AGX Hyperion. As a partner, Stellantis will deliver at least 5,000 autonomous taxis to Uber for operations in the U.S. and international markets, while Uber manages end-to-end fleet operations.

Uber Expands Through a Light-Asset Partnership Strategy

Uber’s partnerships and strategy clearly show a highly asset-light operating model. Rather than competing directly in costly Robotaxi R&D, Uber leverages its core strengths—a high-liquidity, cross-regional platform—to maximize the economic efficiency of autonomous driving. By working with autonomous vehicle manufacturers, Uber ensures sufficient Robotaxi supply while lowering operating and commercialization costs.

A hybrid network combining human drivers and Robotaxis is another key advantage. Ride demand is highly volatile, peaking during rush hours and falling sharply off-peak. Relying solely on Robotaxis would require a fleet roughly twice as large to meet peak demand, leading to significant idle capacity during off-peak hours and poor capital efficiency.

In a hybrid model, human drivers can flexibly come online during peak periods to fill supply gaps, while Robotaxis handle demand during off-peak hours. This structure boosts vehicle utilization and strengthens platform pricing power. Given the high capital cost of Robotaxis, utilization—rather than unit cost—is the key driver of economic returns.

Under this model, pricing power remains centralized within Uber’s platform. Prices are determined by Uber’s dynamic pricing algorithms; human drivers act as price takers, choosing whether to accept rides. Robotaxis, as directly dispatchable supply, can rapidly supplement peak demand and replace part of human supply during off-peak hours. While greater supply substitutability weakens drivers’ bargaining power, Uber uses Robotaxis as a buffer—combined with targeted subsidies and dynamic dispatch—to manage driver attrition without disrupting market equilibrium. Short-term friction may exist, but Uber’s long-term control over pricing and network effects remains intact.

Competition and Risk Analysis

Market concerns around Uber’s autonomous driving business focus on two main issues: the upfront capital required for partnerships may pressure early margins, and Uber’s reliance on partners for autonomous vehicles could pose risks if those partners choose to launch their own apps and bypass Uber.

However, in the foreseeable short to medium term, autonomous driving cannot fully replace ride-hailing. Robotaxis are currently concentrated in short urban trips; longer distances, suburban routes, and complex scenarios still require human drivers. Even companies like Waymo and Tesla, which operate their own apps, face challenges managing consumer operations independently at scale. As a result, Uber remains a central mobility provider.

Waymo Still Relies on Uber’s Platform to Acquire Riders and Boost Utilization

By the end of 2025, Waymo was completing around 450,000 rides per week, or about 6 million per quarter, with a portion coming via Uber in Austin and Atlanta. Even if Waymo reaches an estimated 1 million weekly rides in 2026, that would still represent only about 0.4% of Uber’s roughly 38 million daily trips globally—posing limited threat to Uber’s overall business.

High capital expenditures, R&D, operations, and customer acquisition costs keep Waymo unprofitable. Operating independently would require significant investment in customer service, fraud prevention, dispute handling, and account management. In cities like Los Angeles and Phoenix, Waymo requires users to download its own app, but in other markets it relies entirely on Uber, giving up direct brand exposure. This underscores that even the Robotaxi leader cannot yet operate fully independently of Uber. While Waymo could eventually steer users to its own app, over the next 5–10 years it is still likely to rely on Uber’s platform to maximize utilization.

Tesla Faces Regulatory Scrutiny, Delaying Commercialization

Progress on Tesla’s Robotaxi remains uncertain. Beyond limited pilot operations in Austin last June—still requiring safety monitors—test results revealed system anomalies and operational errors, creating risks for U.S. commercialization timelines.

Tesla faces even greater challenges overseas. While Waymo has expanded testing to London and Tokyo and plans commercial services in London this year, Tesla’s Full Self-Driving (FSD) technology is under strict scrutiny by EU and UK regulators. The Dutch vehicle authority (RDW) has publicly denied Tesla’s claim that FSD would receive EU approval by February 2026. Europe’s conservative regulatory stance further dims prospects for FSD commercialization.

By contrast, Uber has announced multiple partnerships to launch Robotaxi pilots and commercial services across Europe. Its asset-light approach and collaboration with technology providers—such as Wayve, with plans for public-road L4 testing in London this year—stand in sharp contrast to Tesla’s regulatory hurdles.

In China, Tesla has only received partial approval for “intelligent assisted driving” (IAD). China is the world’s largest commercial Robotaxi and ride-hailing market, making scale critical. Tesla’s delayed progress and regulatory constraints there pose structural risks, especially as local players like Baidu Apollo Go, Pony.ai, and WeRide expand rapidly.

Uber’s Role as a Demand-Supply Aggregator Remains Central

Uber’s massive user base—189 million MAPCs across 70 countries and 15,000 cities—represents a demand network built over many years.This scale attracts autonomous driving companies seeking deployment. The market is unlikely to support numerous standalone Robotaxi apps. Instead, it will likely feature a mix of companies focused on technology, others on direct services, and those prioritizing utilization through platform partnerships. Uber naturally fits the role of aggregating both supply and demand, leveraging network effects for competitive advantage.

Robotaxi adoption is expected to take 10–30 years. Near-term penetration remains limited, with North American autonomous vehicle market share projected to rise from 0.9% in 2026 to 7.5% in 2030. Even as competitors expand, Uber retains room to grow market share and users. Through diversified partnerships with Volkswagen, BYD, Lucid, Stellantis, and others, Uber can ensure continued autonomous vehicle supply, reducing dependence on any single provider. Even if Uber is no longer the dominant player in the long run, it is unlikely to be fully displaced by Waymo or Tesla.

Conclusion

Overall, the operating strategies and partnerships adopted by Uber and autonomous vehicle makers suggest that Robotaxi development will continue toward a hybrid model combining self-operated services and platform partnerships.

Beyond proprietary Robotaxi platforms, ride-hailing companies like Uber bring vast user bases, multi-country operations, and extensive driving data—critical growth catalysts in the early stages of Robotaxi commercialization. Given the high cost of autonomous vehicles, maximizing utilization is essential. High-liquidity, wide-reaching platforms that integrate supply and demand can unlock the strongest economic returns. During peak periods, Robotaxis and human drivers can work together to meet demand; during off-peak hours, Robotaxis can substitute for surplus human supply, supporting higher pricing power and utilization.

As a result, hybrid networks on ride-hailing platforms are likely to be a key pathway for rapid Robotaxi growth. Automakers without the ability to build consumer-facing platforms can still profit by supplying hardware, technology, or software licenses, leaving end-to-end fleet management to platforms like Uber. The future Robotaxi landscape is likely to evolve into a non-exclusive, open ecosystem—where some players focus on technology, others on direct services, and many collaborate with platforms to maximize utilization and returns.

Related Artilce