M&A Rationale

Netflix is the world’s leading subscription-based streaming entertainment platform, with core offerings spanning TV series, films, and games. As of the end of 2024, Netflix had approximately 302 million paid subscribers, with services available in more than 190 countries and regions, giving it a highly globalized user base.

Related Articles: U.S. Stock Market 101: Introduction to Netflix’s Business

Netflix’s Two Key Growth Drivers: Subscribers and ARPU

The revenue structure of streaming platforms is essentially determined by “number of subscribers × average revenue per user (ARPU).” The growth momentum of these two factors directly drives mid- to long-term revenue and cash flow performance.

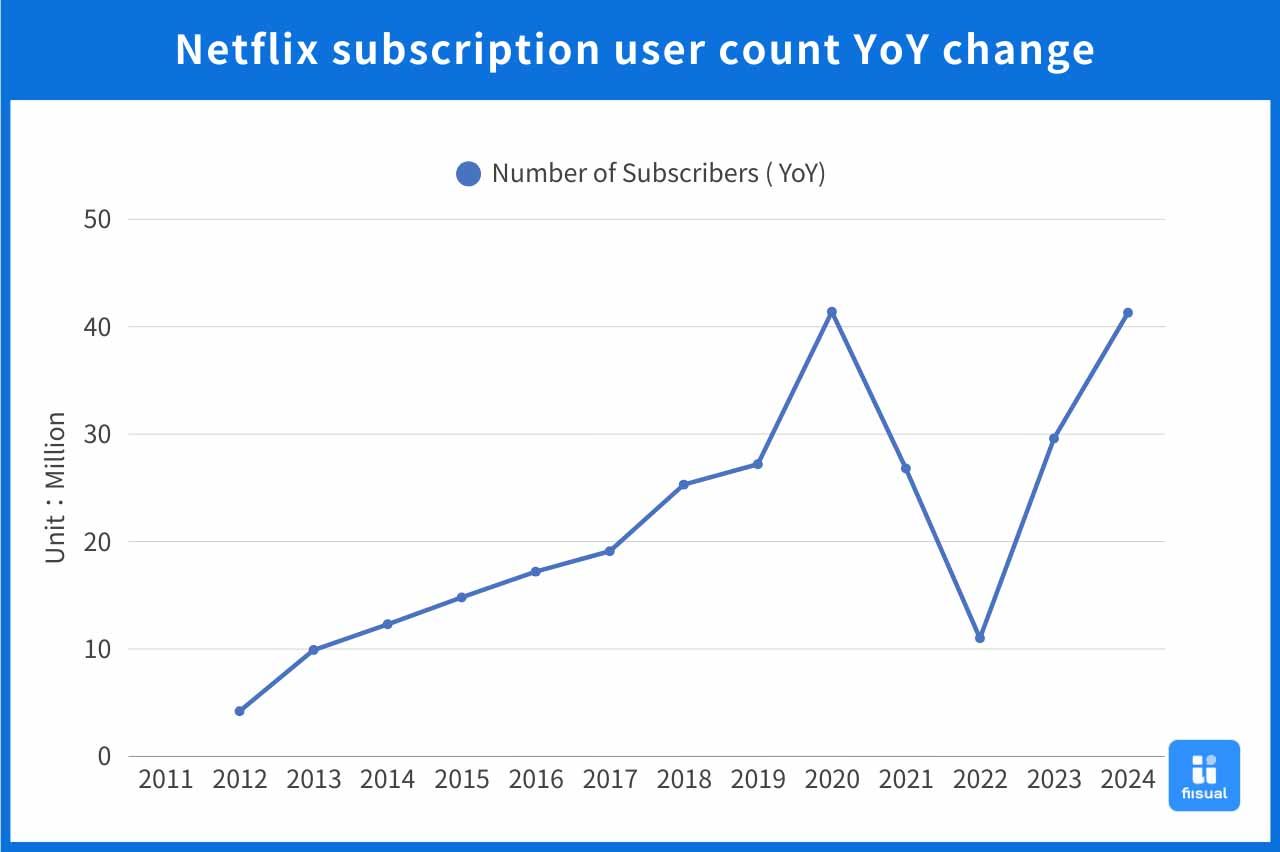

In recent years, Netflix’s subscriber growth has clearly slowed. The company has converted some potential users into paying subscribers by cracking down on password sharing, and has also launched lower-priced, ad-supported plans to attract price-sensitive users while opening up new advertising monetization channels. These strategies are primarily aimed at expanding the subscriber base. However, subscriber growth will eventually peak. Netflix has announced that starting in 2025 it will no longer disclose total subscriber numbers on a quarterly basis, which the market has interpreted as an implicit signal of slowing user growth momentum.

As a result, the company’s future operational focus is expected to shift toward increasing ARPU. ARPU growth could be driven by higher ad penetration or AI commercialization models, but so far there are no concrete, quantifiable results. In the short term, if Netflix can secure a large portfolio of IP assets and enhance its pricing power—extending IP lifecycles through multi-channel exposure (both online and offline)—this may be one of the fastest ways to generate tangible results.

Against this backdrop, Warner Bros. Discovery’s willingness to divest part of its core businesses aligns well with Netflix’s need to rapidly expand its commercial footprint. Warner Bros. Discovery owns globally recognizable, long-lived IP such as the DC Universe, Harry Potter, and Game of Thrones. In addition, it has a mature production system and theatrical distribution capabilities. A merger between the two companies could create potential synergies by expanding revenue sources while reducing content production and acquisition costs.

After Paramount’s series of attempted acquisitions failed to materialize, Netflix formally submitted an acquisition proposal to Warner Bros. Discovery on November 20, 2025.

On December 5, Netflix announced that it had reached a preliminary agreement with Warner Bros. Discovery and entered an exclusive negotiation period. The transaction was initially structured as a combination of cash and Netflix stock. On January 20, 2026, Netflix announced that it would switch to an all-cash acquisition and submitted a preliminary proxy statement to the U.S. Securities and Exchange Commission (SEC). The offer price is USD 27.75 per Warner Bros. Discovery share, implying an equity value of USD 72.0 billion and an enterprise value of USD 82.7 billion—a significant premium of 121.3% over the undisturbed share price as of September 10.

The transaction targets the Streaming and Studios-related assets retained by Warner Bros. Discovery, including Warner Bros. Studios, HBO and HBO Max, and their core content and IP portfolio. Linear cable network assets such as CNN will be spun off into Discovery Global prior to the transaction’s completion. The companies have indicated that closing is expected within 12 to 18 months, subject to completion of the spin-off and receipt of necessary regulatory approvals and shareholder consent. If the deal is ultimately terminated due to regulatory rejection, Netflix will pay a breakup fee of approximately USD 5.8 billion, underscoring its strong strategic commitment to the transaction.

Table: Timeline of the Warner Bros. Discovery Sale Process

| Date | Development |

|---|---|

| 2023/12/19–20 | Warner Bros. Discovery CEO David Zaslav met with Paramount CEO Bob Bakish in New York, initiating discussions on potential M&A. Topics included synergies from integrating Max and Paramount+, as well as evaluating mergers or consolidation to improve cost efficiency. |

| 2025/06/09 | Warner Bros. Discovery announced plans to split its business into two segments—streaming & studios, and cable networks—laying the groundwork for potential transactions. |

| 2025/09/11 | Media reports indicated that Paramount was preparing a bid. Following the news, WBD shares surged nearly 30%. |

| 2025/09/14–2025/10/13 | Paramount submitted three consecutive offers ($19 / $22 / $23.5 per share). Warner Bros. Discovery rejected all bids, stating that any acceptable offer would need to exceed $30 per share. |

| 2025/10/21 | After receiving an unsolicited offer, Warner Bros. Discovery announced the launch of a strategic review, considering the sale of all or part of the business rather than limiting options to a breakup. |

| 2025/11/20 | Netflix, Comcast, and Paramount each submitted formal acquisition proposals ahead of the deadline. |

| 2025/11/25 | Warner Bros. Discovery requested revised bids from all parties by December 1 to advance to the next round of screening. |

| 2025/12/01 | Deadline for second-round revised bids: Netflix (primarily cash) and Comcast (cash/equity) advanced to the next round for the streaming and studio assets. |

| 2025/12/08 | Paramount Skydance launched a hostile all-cash tender offer directly to shareholders at $30 per share. |

| 2025/12/17 | Warner Bros. Discovery cited insufficient financing and conditions from the opposing bid and reiterated its support for Netflix’s proposal. |

| 2025/12/22 | Larry Ellison provided a personal guarantee totaling $40.4 billion, addressing financing concerns, and extended the offer period to January 21, 2026. |

| 2026/01/07 | Warner Bros. Discovery again rejected Paramount Skydance’s acquisition offer. |

| 2026/01/20 | Netflix announced a switch to an all-cash acquisition structure and filed a preliminary proxy statement with the U.S. Securities and Exchange Commission (SEC). |

Synergies from the Acquisition

After the merger, the core revenue expansion logic lies in addressing Netflix’s long-standing weakness in its content asset structure. Netflix’s original content has often been characterized by one-off hits, lacking long-running, serializable IP that can be extended across multiple media formats. In contrast, Warner Bros. Discovery’s IP—such as the DC Universe, Harry Potter, and Game of Thrones—exhibits strong compounding characteristics.

Integrating these IP assets into Netflix’s ecosystem could shift content investment from a highly uncertain, one-off hit-driven model toward a sustainable, repeatable IP management model. This would help attract core fan bases, strengthen content differentiation, enhance pricing power, and support mid- to long-term ARPU growth.

Games are also an important tool for extending IP popularity and deepening monetization. Netflix currently positions games more as an extension of platform functionality, experimenting with use cases such as TV party games. While downloads and reach have improved, games still contribute less than 0.5% of total user time spent on the Netflix platform, indicating that they are not yet a key driver of retention or engagement.

By contrast, Warner Bros. Discovery has demonstrated more mature commercial validation in IP-based gaming, with successful titles such as Suicide Squad: Kill the Justice League and Hogwarts Legacy. The company has recognized that most game projects struggle to generate stable profits and has therefore strategically concentrated resources on four core IPs, aiming to reduce earnings volatility, improve hit rates, and enhance overall capital efficiency. Overall, Warner Bros. Discovery’s experience and execution in gaming are clearly superior to Netflix’s and offer valuable lessons that Netflix could replicate.

In addition, post-merger, Netflix’s global distribution capabilities and algorithmic recommendation advantages could complement Warner Bros. Discovery’s mature large-scale production management system and theatrical release windows. This would allow a single IP to capture both box office revenue and long-tail streaming monetization, extending the economic lifecycle of content assets, diversifying recovery channels, improving overall content IRR, and reducing reliance on any single distribution model—positively impacting mid- to long-term earnings stability.

Table: Warner Bros. Discovery Content Pipeline

| Category | Title | Expected Release | Notes |

|---|---|---|---|

| Series | Harry Potter (TV series) | Launch in 2026, planned for 7 seasons | Re-adaptation based on the original novels; the original Harry Potter film franchise generated over $7.7 billion in global box office revenue |

| A Knight of the Seven Kingdoms | January 8, 2026 | A spin-off within the A Song of Ice and Fire universe | |

| Films | Supergirl | 2026 | Part of the DC content strategy; Superman films within the same universe generated approximately $616 million globally |

| Clayface | 2026 | Directed by James Watkins, known for directing episodes in Black Mirror Season 3 | |

| The Cat in the Hat | 2026 | Directed by Alessandro Carloni, whose notable works include Kung Fu Panda 3 | |

| Superman 2 | 2027 | Continuation of the Superman film series; the previous installment earned approximately $643 million worldwide | |

| Gremlins | November 19, 2027 | Reboot of a classic IP; the 1984 Gremlins film grossed around $150 million globally | |

| The Lord of the Rings: The Hunt for Gollum | December 17, 2027 | Based on story elements from J.R.R. Tolkien’s The Lord of the Rings universe |

Cost Synergies

Netflix management has stated that starting in the third year after completion, the transaction is expected to generate at least USD 2–3 billion in annual cost savings. These synergies can be reasonably broken down into four main areas:

- Bandwidth cost optimization: Integration of streaming technology infrastructure, unified servers, networks, and content delivery networks, reducing redundant investments and improving bargaining power with cloud service providers. App development and technical teams can also be consolidated to avoid duplicated functionality.

- Content production and IP management: Unified procurement and larger production scale could lower unit production costs. Shared studios, post-production facilities, and technical staff would reduce idle capacity and duplicate investments. Content planning could focus more on high-value, long-lived IP while leveraging both libraries for spin-offs.

- Marketing and user acquisition: A combined user base would enable unified acquisition channels and strategies, reducing duplicate marketing spend and improving bargaining power with advertising platforms. Cross-promotion within Netflix could further improve conversion efficiency.

- Organization and human resources: Integration of global offices and back-office functions such as finance, legal, and HR could reduce overlapping roles, lower fixed personnel costs, and improve operational efficiency.

Key Risks

Financial Considerations

The consideration for this transaction is set at $27.75 per share, structured as an all-cash acquisition, implying an equity value of $72.0 billion. From a funding perspective, Netflix currently holds approximately $13.0 billion in cash and cash equivalents, which is clearly insufficient to cover the full cash consideration. To address this gap, Netflix has secured around $67.2 billion in bridge financing commitments from financial institutions including Wells Fargo. In addition, the company initiated refinancing efforts in late December 2025, obtaining a $5.0 billion revolving credit facility and two delayed-draw term loans of $10.0 billion each. After these arrangements, approximately $42.2 billion of the original bridge financing commitments still need to be syndicated through the loan market (i.e., roughly $25.0 billion in long-term debt and $42.2 billion in short-term bridge financing commitments).

Next, assessing Netflix’s total debt post-transaction: Netflix currently carries approximately $13.5 billion in long-term debt. This will be supplemented by roughly $67.2 billion in new acquisition financing, as well as the assumption of approximately $10.7 billion in existing Warner Bros. Discovery debt, inferred from an enterprise value of $82.7 billion minus $72.0 billion in equity value. In aggregate, Netflix’s pro forma total debt would rise to approximately $91.4 billion, significantly increasing leverage and potentially exerting pressure on interest expenses and credit ratings.

Turning to whether operating cash flow (OCF) can cover current liabilities: assuming, on a simplified basis, that post-merger OCF is the direct sum of both companies, combined annualized OCF would be approximately $15.0 billion (Netflix at around $11.0 billion plus Warner Bros. Discovery at approximately $6.0 billion). On the liabilities side, Netflix’s existing current liabilities are about $11.0 billion. Adding the $42.2 billion of bridge financing that has yet to be refinanced brings total current obligations to approximately $53.2 billion. Under this scenario, the OCF-to-current-liabilities ratio is roughly 0.28, indicating that Netflix would be clearly unable to repay all short-term obligations within 12 months using operating cash flow alone. That said, the capital structure of large-scale acquisitions is not designed to rely on single-year OCF for principal repayment. Instead, short-term debt is typically rolled over and refinanced into longer-term instruments to spread maturity risk over time. Within this framework, the more critical question is not whether OCF can fully repay principal, but whether interest coverage can remain stable. A more definitive assessment will depend on the final debt structure and interest rate terms. However, if the acquisition results in a downgrade of Netflix’s credit rating, future borrowing costs would rise further (Netflix is currently rated A3 by Moody’s and A by S&P).

- From a subscriber perspective, there is significant overlap between the two platforms in the U.S. market. According to estimates by Antenna, as of October 25, 2025, approximately 10.6 million households subscribed to both Netflix and Max, representing about 45.2% of Max’s subscriber base. This high degree of overlap means that post-merger synergies will depend heavily on the execution of bundle integration, pricing strategies, and content programming, all of which carry meaningful uncertainty.

- Demand in the theatrical exhibition market is also trending downward. This decline is structural rather than cyclical and cannot be reversed solely through Netflix’s operational integration. Moreover, if Netflix shortens the theatrical release window before films move to streaming post-acquisition, this could further pressure already weakened box office revenues.

- Warner Bros. Discovery’s revenue trajectory has been declining. The company reported revenues of $41.3 billion in 2023 and $39.3 billion in 2024, equivalent to approximately 123% and 102% of Netflix’s revenue, respectively, indicating that WBD’s revenue base remains larger than Netflix’s. However, over the same periods, net income stood at –$3.1 billion and –$11.3 billion, equivalent to –58% and –130% of Netflix’s net income, underscoring weak profitability. The primary drivers are continued declines in studio production and cable television revenues. While growth in streaming subscriptions has partially offset these pressures, the effectiveness of integrating these businesses remains uncertain.

Feasibility Analysis

In 1Q25, Netflix and HBO Max held approximately 20% and 13% of the U.S. SVOD market, respectively. A combined market share exceeding 30% could trigger antitrust scrutiny under U.S. Department of Justice thresholds. Beyond regulatory risk, Paramount has raised procedural fairness concerns, suggesting potential litigation and shareholder-related uncertainties.

That said, such an acquisition is unlikely to fundamentally disrupt industry competition. IP expansion tends to offer temporary or phased advantages rather than structural change, as seen in Disney’s acquisition of 21st Century Fox and Amazon’s acquisition of MGM. Absent major political or policy intervention, the deal’s feasibility remains relatively favorable.

Brief Commentary

Entering the transaction analysis, this deal represents a hybrid of horizontal and vertical integration. Netflix’s long-standing weakness has been the lack of evergreen, cycle-resilient IP that can be repeatedly monetized over time. Warner Bros. Discovery’s core value, by contrast, lies in its century-old content library and mature production system—particularly IP such as DC, which carries strategic importance for any major platform. By combining Netflix’s platform distribution and data capabilities with Warner Bros. Discovery’s content assets and production infrastructure, the merged entity has the potential to form a closed loop across production, distribution, and monetization, while lowering costs through vertical integration.

That said, this same dynamic also introduces risk. Should Netflix move closer to a dominant position, it could gain stronger bargaining power over content acquisition pricing and production budgets, potentially compressing compensation for creators such as writers and actors. Moreover, Netflix has historically favored shorter theatrical windows and faster transitions to streaming. If this approach were applied to Warner Bros. Discovery’s established theatrical distribution model, it could trigger pushback from theater operators and intensify strategic friction within Hollywood.

Looking ahead, we believe investors should continue to focus on three key questions:

- After adding approximately 128 million users to its subscriber base, how will Netflix use pricing, tiered plans, and content allocation to precisely lift ARPU, rather than merely pursuing scale expansion?

- With the integration of century-old, long-duration IP, how will Netflix build new content universes and leverage AI-enabled production workflows to drive further structural transformation across the industry?

- In the face of WBD’s existing offline distribution and theatrical systems, how will Netflix efficiently reuse these channels to create an ecosystem based on resource sharing rather than internal conflict?